How will the Proposed Regulatory Changes Impact the Housing Industry?

A lot of home builders are thrilled at the possibility of being able to build without all those “regulatory headaches”. Comments from some of them in this article indicate many are absolutely giddy.

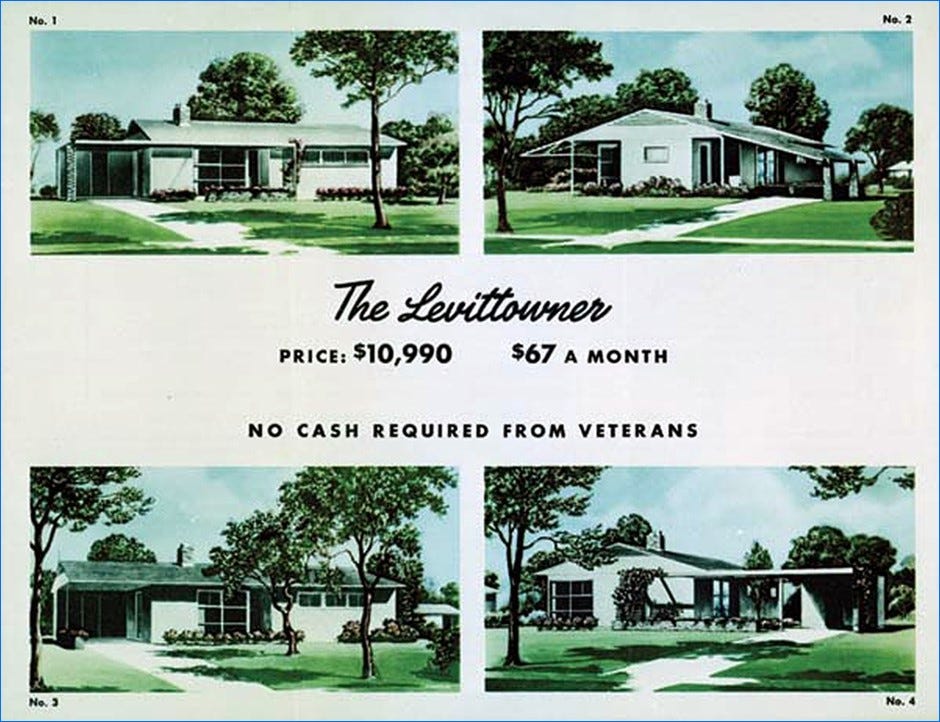

To review, there is too much demand, and not enough supply, in terms of housing stock. And that’s magnified when we think about starter houses. Back in the 1950’s, depending on whose statistics you believe, between 13 and 15 million starter houses were built. Now, that number is miniscule, and the houses are bigger and less affordable. Are you old enough to remember the Levittowns? Some history (with videos).

These houses were tiny compared to most houses today. They started, originally, at about 750 sf, and eventually grew to about 1,400 sf. And they were “big enough” for a family - and since this was generations before House Hunters, everyone shared one bathroom, and there was no granite.

The Levittown communities, and similar building developments, were places where veterans could leverage the GI bill, buy a house on one income, have a family, and live in a community1. It was the Silent Generation who bought these houses, and Boomers who grew up in them. They eventually moved to bigger houses, and these starter houses enabled others to start their journey to homeownership.

Some history on how this ceased to exist. At base: land prices skyrocketed, people wanted larger and fancier houses, the price of building materials and construction worker wages kept going up, and there were more permits required.

The last point, about permits, is what the incoming regime wants to change.

A lot of people want to own a house because LAND is a limited commodity. There is only so much land, and not all of it is good for building houses. Over the years, more and more regulations have been put in place to keep buildings safer, in terms of both construction and location.

One such regulation prohibits building homes near water, or roadside drainage ditches that connect to creeks and streams, without first obtaining a federal wetlands permit.

If you think this doesn’t matter, think back to Hurricane Harvey, in 2017. Thanks to a complete lack of important regulations, a dearth of updated floodplain maps, and the fact that Texas ignores most regulations, 209,422 of Houston’s 501,721 homes had some kind of damage. 40% were in a floodplain. 30,000 people were displaced. That’s just one example.

And then there’s Florida. In addition to losing coastline to climate change, increases in daily flooding due to groundwater, and a lack of regulations, a lot of those people who moved to Florida because “no taxes” are facing huge HOA fees, along with outrageous home insurance rates. Those rates are exclusive of flood insurance, which must be secured separately.

You get the idea: many home builders are in it for the money, prefer to build with “builder grade” materials2 to maximize profits, and since they leave when the home is sold, couldn’t care less about what happens next.

So perhaps they will be able to leverage the end of flood restrictions, along with the end of having to meet energy efficiency standards, and build a ton of houses. But will their commitment to quick and cheap translate into livable homes?

Unlikely. Think leaking roofs from cheaping out on the flashing and roof crickets. Think water infiltration in the walls. Think mold. Think higher monthly utility charges due to a lack of insulation and other energy efficiencies. And then, when the owners try to sell, lower resale values because of things like “luxury vinyl plank” flooring, cheap cabinets, and potentially problems with electrical wiring and plumbing.

And that’s before the houses sink, flood or face other environmental disasters.

Location, location, location.

There are really good reasons to have permit requirements, environmental requirements, and other legal requirements. The fascist regime “promise” is that without the regulations, it will be possible for builders to construct more homes, and more affordable homes.

Doubtful.

To buy a house, one must secure a mortgage and insurance. While the new fascist regime doesn’t care about regular people, only about making money; banks and insurance companies have other concerns. Will new houses be able to be appraised at the list prices? If not, the buyers will need money above the mortgage amount they can acquire. Will the insurance companies agree to insure houses that are doomed to failure?

Unlikely.

And that’s not to mention which humans will physically build the houses. Depending on whose numbers you believe, between 20 and 30% of construction workers nationwide are undocumented. So, they may stay home in the face of potential raids. Legal immigrants (another chunk of construction workers) may live in mixed households and may also stay home. So, the companies will need to find “American” construction workers. In 2024, there was a shortage of about half a million construction workers. Obviously, this number would grow if there are deportations. To get these employees, the construction companies will need to raise wages, and even that may not be enough if there aren’t enough capable workers. That would either causes prices to rise above any savings from rolled-back regulations, or they’d make less profit.

Let’s circle back to the original definition of the housing problem: too much demand and not enough supply. Will doing away with regulations increase supply enough to meet demand?

Nope.

Having “enough” supply does nothing to answer to demand if the new housing is substandard or unaffordable, or if the type of housing does not match the needs of the buyers.

A word on “affordability”. Think back to 2005 - 2006. Virtually anyone could get a mortgage, potentially a balloon mortgage. Brokers allowed for people with, say, $40,000 in annual income to qualify for a mortgage of, say, $400,000. We all remember when the housing bubble burst in 2007-2008 due to the bankruptcy of a lot of sub-prime lenders due to the fact that no one earing $40,000 a year can afford a $400,000 mortgage. Tour down memory lane. The housing sector has not yet recovered from that.

In October 2024, the median cost of a house in the US was slightly over $400,000 but that varies widely on a state-by-state basis. Let’s pretend that the removal of the regulations saves 10% on the cost of a house, bringing it down to a median of $360,000. Has housing become more affordable?

If a buyer put down 20% of the house value, that would decrease the required amount from $80,000 to $72,000. Not a huge difference. Granted, buyers can leverage various programs to allow for a smaller downpayment, if those programs still exist under the new fascist regime. A lower downpayment increases the monthly payment, but with a less than 20% downpayment, the buyer will need PMI (private mortgage insurance) to satisfy the bank underwriting requirements.

Median household income varies greatly by geography, gender, race, and educational attainment. It fell from 2022 to 2023, and numbers for this year are not out yet. But the rule of thumb is that one’s cost of housing should be under 30% of their household income.

My math: I used this mortgage calculator for a $360,000 mortgage, with a 20% downpayment, and the monthly cost was $2,404. To stay at 30%, that would be an annual income of $96,106. Using the same calculator with a 10% downpayment yields a monthly cost of $2,842, or an annual income of $113,680. Trust me, above median incomes at all levels.

You could potentially make the case that the new houses would encourage people with large houses to downsize, and then their houses would be available. But that’s only if the builders concentrate on the houses that Boomers want3 which would make them less money than building larger houses.

Gee, kinda sorta make you wish that the candidate who would have helped first time homebuyers with $25,000 in downpayment assistance would have won.

Yes, this was mostly white people due to redlining and discrimination.

These are things like flooring, cabinets, finishes, etc., that are inexpensive, and prioritize cost over quality.

They are the primary owners of the kind of houses that would be downsized. Many Boomers are in 4-bedroom houses, and would downsize IF the new house cost less, was on one floor, and met the needs for aging in place.

There is a definite housing boom here in Beaverton, Oregon. New rules that allow duplexes, triplexes, quadplexes, townhomes, and cottage clusters in Beaverton’s residential neighborhoods took effect in June 2022. There are 5 story apartment/condo complexes going up all over - many with ground floor retail. Much of it is redevelopment on former retail space, although some is new construction on open space. How much is actually "affordable" is open to discussion - depending on location.

The problem here with the older "silent generation-bought" housing, is much of it is literally falling apart. Mold is rampant, poor insulation, and 70 years of wear and tear on cabinets, floors, and counters, has taken its toll. Wall heaters are not efficient, windows are all single pane and not efficient... It becomes easier to tear down and start over, than to try and bring them up to standards of today.

How would low rise, affordable condos or rental apartments affect your cogent analysis?